.png)

Introduction

Every company wants to reduce its AWS bill, and choosing the right commitment term is one of the most reliable ways to achieve it. But deciding between a 1-year and 3-year AWS Savings Plan isn’t as simple as comparing discount percentages

Workloads change, architectures evolve, and a single misjudgment can lock you into terms that no longer match how your environment actually runs.

AWS does provide automated recommendations in the console, but those suggestions don’t always reflect your unique usage patterns, roadmap, or risk tolerance.

This guide breaks down the major factors you need to consider while choosing between 1-year and 3-year Savings Plans. It also breaks down the math for you, the risks, and the practical decision frameworks which you can use to choose the ideal commitment term that fits your business.

Quick Answer: When to Choose 1-Year vs 3-Year AWS Commitments

When deciding between a 1-year vs 3-year AWS commitment, the fastest way to get clarity is to evaluate how stable your workloads are and how much flexibility you need.

You should choose a 1-Year AWS Commitment, if:

- Your workloads change frequently: You are expecting migrations, refactors, or architecture shifts in the next 12–18 months.

- Your usage is volatile: Your platform experiences monthly swings or seasonal patterns >20–25%.

- You rely on rapidly evolving services, such as databases, managed data platforms, or new serverless layers.

- You need budgeting flexibility, especially for growing companies or teams with dynamic roadmaps.

- You want to re-evaluate commitment coverage every year to match shifts in infrastructure.

You should choose a 3-Year AWS Commitment, if:

- Your compute baseline is stable: You fit well in long-lived EC2 workloads, steady container clusters, or predictable backend services.

- You want the highest possible AWS term savings, typically the largest discount available.

- Your architecture changes slowly, with no major modernization efforts planned.

- You’re optimizing for long-term cost reduction and can tolerate reduced flexibility.

- Your variance is low: Your monthly usage typically fluctuates <10–15%.

You should choose a Mixed-Term Strategy, if:

- Your baseline is stable, but your peaks and new workloads fluctuate.

- You want the stability of 3-year coverage for the core, and the flexibility of 1-year for emerging services.

- Your team prefers to increase commitment coverage gradually rather than all at once.

In summary, the choice is a commitment term comparison based on:

- Volatility: How predictable your usage is

- Roadmap certainty: Upcoming migrations, Graviton shifts, or service changes

- Baseline stability: Steady compute vs dynamic workloads

- Discount preference: Comfortable with paying less with 3-year or reduce risk with 1-year

We have broken down each of these factors with formulas, examples, and scenarios to help you make the right choice.

AWS Commitment Terms Explained: The Technical Differences Between 1-Year and 3-Year Savings Plans

To choose between a 1-year vs 3-year AWS commitment, you need to understand exactly how AWS structures its products. While both commitment durations fall under the umbrella of AWS Savings Plans or Reserved Instances, the term length affects far more than just the size of your discount. It changes how much flexibility you have, how much risk you carry, and how confidently you can align commitments with your infrastructure roadmap.

Below is a breakdown of what truly changes between 1-year and 3-year terms.

This means:

A 1-year term can tolerate roadmap changes; a 3-year term assumes your baseline architecture stays stable for years.

This becomes critical for teams predicting refactors, modernizations, or migrations.

Also read: AWS Savings Plans vs Reserved Instances: A Practical Guide to Buying Commitments

Discount Mechanics: Why Term Length Changes Your Effective Rate

The reason 3-year commitments deliver dramatically higher AWS term savings is because AWS values long-term predictability.

AWS internally prices 3-year commitments to:

- Increase revenue certainty

- Decrease resource planning risk

- Offset potential infrastructure footprint fluctuations

As a result:

- 3-year SPs often deliver 2x the incremental discount compared to 1-year SPs.

- For RIs, the delta can be even larger due to specificity (region, instance family, tenancy).

Even without citing exact percentages, the structural difference is unambiguous:

- The 3-year plan offers the highest discount but also the highest risk.

- The 1-year plan offers moderate discount but it is adaptable to change.

Flexibility Differences: Where 1-Year and 3-Year Behave Very Differently

AWS Savings Plans come in two primary plans:

Compute Savings Plan (CSP)

It applies broadly across EC2 instance families, sizes, regions, OSes, Fargate, and Lambda.

- 1-year CSP: It is easy to align with evolving architectures

- 3-year CSP: It is only safe when infrastructure is predictable

EC2 Instance Savings Plan (ISP)

It is more restrictive and less flexible, but it offers better discounts

- 1-year ISP: It is a better choice for predictable workloads

- 3-year ISP: It comes with high-risk, if instance family or region changes

Reserved Instances (RIs) on the other hand are specific to region, instance family, tenancy and platform. Though convertible RIs soften the rigidity, they still require staying within a compatible compute family.

3-year RIs will carry the most regret potential, if:

- you move to containers

- you adopt Graviton

- you change storage or compute profile

- you shift regions

- instances are rebalanced by autoscaling or orchestrators

1-year terms significantly reduce this regret risk.

Operational Constraints: Why 3-Year Terms Are Harder to Undo

Once you commit:

- You cannot “return” unused commitment

- You cannot downgrade commitment terms

- You cannot change term length after purchase

- AWS won’t auto-correct if usage drops

- You are locked into the hourly commitment amount regardless of consumption

Also read: Cut Your Azure Bill by 40% in 5 Minutes: The Complete Setup Guide

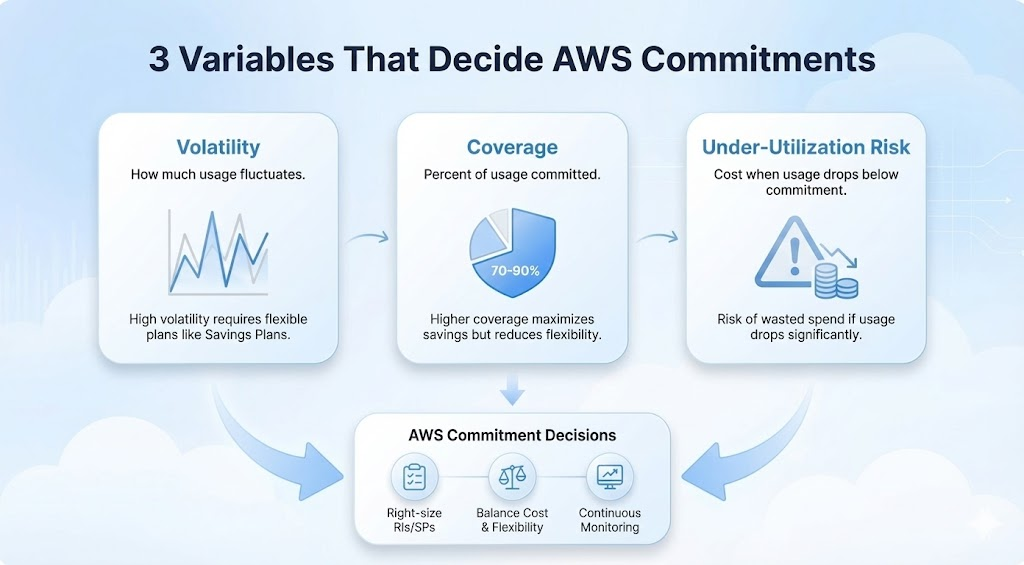

The Three Variables That Decide AWS Commitment Terms: Volatility, Coverage, and Under-Utilization Risk

Regardless of which AWS Savings Plan or Reserved Instance type you’re evaluating, three variables ultimately determine whether a commitment will generate savings or create financial drag:

- Volatility: how much your usage swings

- Coverage: what % of your environment you commit to

- Under-Utilization Risk: the dollar impact if usage drops

Understanding these variables is the foundation of any accurate commitment term decision. This section breaks down each one with the precision needed for finance, FinOps, and engineering teams to make long-term decisions confidently.

1. Volatility: How Predictable Is Your Usage Over Time?

Volatility measures how much your compute usage fluctuates month-to-month. It is the single most important variable when comparing 1-year vs 3-year AWS commitments, because long-term terms usually amplify usage deviations.

How to interpret volatility in AWS compute usage:

- Low Volatility (<10–15%): It indicates a stable baseline (e.g., mature backend services, long-lived EC2 nodes)

- 3-year commitments are usually safe

- Medium Volatility (15–25%): It indicates moderate, seasonal, or growth-related fluctuations

- 1-year commitments or mixed-term strategies are usually better.

- High Volatility (>25–30%): It indicates unpredictable usage (e.g., refactors, migrations, or startup growth curves)

- 3-year commitments carry significant regret risk.

The bottomline: If you commit to $100 of hourly spend but only use $60, you pay for the full $100. The longer the term, the more “usage drift” compounds financially.

2. Coverage: What Percentage of Usage You Lock Into Commitments

Coverage determines how much of your total compute footprint is protected by discounted commitment rates.

Coverage = (Committed Spend ÷ Total Compute Spend) × 100%

How coverage impacts decision safety:

- Low Coverage (20–40%): It offers low commitment risk, but there is room to grow.

- 3-year terms can be safe even with moderate volatility.

- Moderate Coverage (40–70%): It offers a balanced risk profile and aligns with most FinOps maturity models.

- Term selection depends on roadmap stability.

- High Coverage (70–90%+): There is a risk of high exposure if usage drops.

- 1-year terms are usually preferred unless volatility is extremely low.

3. Under-Utilization Risk: The Real Cost of Being Wrong

Under-utilization risk is the financial penalty you incur when your actual usage falls below your committed amount. This is the “regret cost” of any AWS Savings Plan or RI.

How under-utilization happens:

- Migrations to containers or serverless

- Database engine changes

- Region expansions

- Traffic downturns

- Architectural modernization (e.g., to Graviton)

- Rightsizing or consolidation

- Product changes that reduce compute demand

So, when your usage drops, you still pay the committed amount, regardless of your actual usage.

Why term length magnifies under-utilization risk:

If a drop happens during:

- a 1-year term; you recover in 12 months

- a 3-year term; the impact compounds over 36 months

How to Calculate 1-Year vs 3-Year AWS Commitment ROI: A Risk-Adjusted Model

Most teams compare 1-year vs 3-year AWS commitments using discount percentages alone, but that method is incomplete and often misleading. You need to rather ask, given the volatility, coverage, and usage patterns, which term will produce the best risk-adjusted ROI?

To answer that, we need a simple, reliable mathematical model that reflects how commitments actually behave in production environments. This section introduces the formulas used by FinOps teams, cloud economists, and advanced purchasing tools to quantify upside, downside, and break-even thresholds.

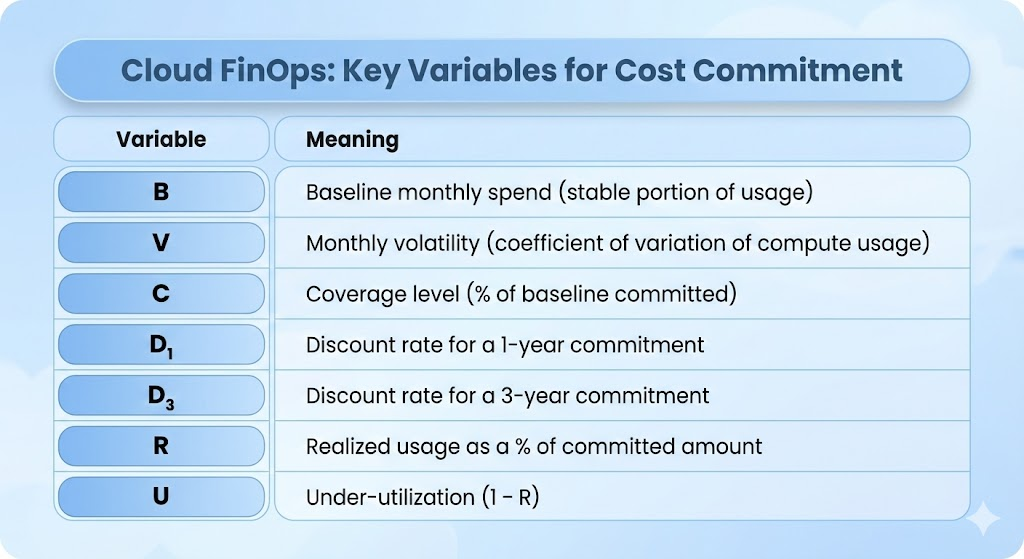

Defining the Variables Used in AWS Commitment Modeling

Let’s start with a simple shared vocabulary. We will be using the variables below to calculate expected savings, downside exposure, and break-even points. Here’s what each variable represents:

Formula 1: Expected Monthly Savings (EMS)

What this formula measures:

This is the “best-case scenario.” It tells you how much money you should save each month if your usage stays consistent with your commitment.

The formula is: EMSi = B x C x Di

Where:

- B = your stable baseline spend

- C = coverage (how much of that baseline you’re committing)

- Dᵢ = discount rate (1-year or 3-year)

Let’s assume:

- Baseline spend (B): $120,000

- Commitment coverage (C): 70%

- 1-year discount (D₁): 20%

- 3-year discount (D₃): 40%

1-Year Expected Savings

EMS1 = 120,000 x 0.70 x 0.20 = $16,800

3-Year Expected Savings

EMS3 = 120,000 x 0.70 x 0.40 = $33,600

What this means:

3-year commitments can get you nearly double the savings, but only if your usage stays stable.

Formula 2: Under-Utilization Cost (UC)

What this formula measures:

This is the real money you lose when your usage drops below your commitment. It captures the financial “regret” of committing too much.

UC = B x C x (1 – R)

Where:

- R = realized usage (% of commitment actually used)

- U = 1 − R = under-utilization

Let’s assume:

- Your usage dropped to 80% of the committed amount

- So R = 0.80 → U = 0.20

UC = 120,000 x 0.70 x 0.20 = $16,800

What this means:

That $16.8K/month is money burned because you overcommitted. If this happens in a 3-year term, you’re stuck with that cost for 36 months, not 12.

Formula 3: Expected Risk-Adjusted Savings (ERAS)

What this formula measures:

This is the real answer to whether a commitment pays off. ERAS subtracts the regret cost (under-utilization) from the best-case savings (EMS).

ERASi = (B x C x Di) – {B x C x (1 – R)}

Let’s assume:

Using the same numbers:

1-Year ERAS

ERAS1 = 16,800 – 16,800 = 0

3-Year ERAS

ERAS3 = 33,600 – 16,800 = 16,800

What this means:

- At 20% volatility, the 1-year commitment breaks even.

- The 3-year commitment still saves money.

But at higher volatility (e.g., 30–40%), the 3-year ERAS quickly turns negative, meaning you lose money overall. This is why companies must factor volatility, not just discount levels.

Formula 4: Break-Even Under-Utilization Threshold

What this formula measures:

This tells you the minimum usage you must maintain for the commitment to remain profitable.

Break-Eveni = 1 – Di

Let’s assume:

For a 1-year commitment

- Discount: 20%

- Break-even usage = 1 − 0.20

- Break-even usage = 0.80 (80% usage required)

What this means:

If your usage drops below 80% of the committed amount, the 1-year Savings Plan stops being profitable.

For a 3-year commitment

- Discount: 40%

- Break-even usage = 1 − 0.40

- Break-even usage = 0.60 (60% usage required)

What this means:

You only need to use 60% of your committed amount for a 3-year plan to break even. But if you drop below that, the losses continue for 36 months, not 12.

Formula 5: Volatility-Adjusted Expected Usage (R_expected)

What this formula measures:

This gives you a reasonable expectation of how much of your commitment you’ll actually consume, based on volatility.

Rexpected = 1 – V

Let’s assume:

If volatility V = 20%:

Rexpected = 1 – 0.20 = 0.80

What this means:

A 20% swing each month means you should expect to use roughly 80% of your commitment over time This helps set realistic savings expectations.

Pulling It All Together: 1-Year vs 3-Year Comparison

Now, let’s plug R_expected into ERAS to see which term performs better after volatility is accounted for.

ERAS1 = B x C x {D1 – (1 –Rexpected )}

ERAS3 = B x C x {D3 – (1 –Rexpected )}

With:

- B = $120,000

- C = 70%

- V = 20%

- D₁ = 20%

- D₃ = 40%

1-Year

ERAS1 = 0 (break-even)

3-Year

ERAS3 = 16,800 (net savings)

What this means:

- At 20% volatility, 3-year commitments still win, but not by much.

- At 30% volatility, 3-year becomes riskier.

- At 40% volatility, 3-year becomes a net loss.

This is why choosing a 1-year or 3-year term feels complex at first. With the right formulas, you can make a structured financial decision rather than getting stuck with the guesswork.

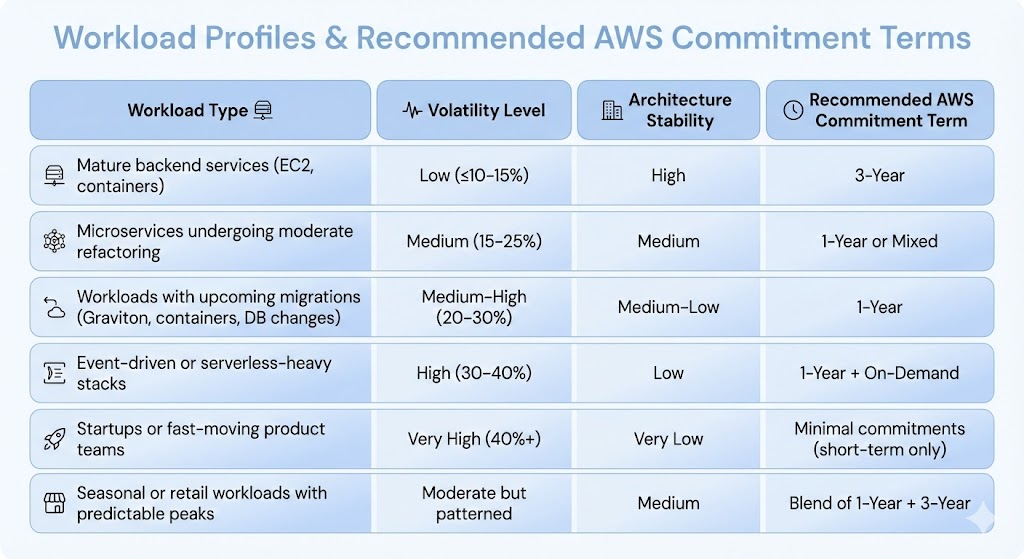

Here are some Recommended Commitment Terms:

Understanding The Regret Curve Where Probability Meets Dollars

When comparing 1-year vs 3-year AWS commitments, the most important consideration is not the discount, but it is the cost of being wrong.

This cost is called regret, and it happens when your usage falls below your committed amount.

The “regret curve” is simply a way to visualize how regret grows as:

- Usage drops, and

- The term gets longer (12 months vs 36 months)

What Regret Actually Means:

Regret = The dollars you lose when you don’t use the compute you committed to.

It is the same formula from earlier:

Under-utilization Cost = B × C × (1 – R)

Let’s assume:

- Baseline (B) = $100,000

- Coverage (C) = 70%

- Usage drop = 20% (R = 80%)

Under-utilization cost = 100,000 × 0.70 × 0.20 = $14,000/month

- Over a 1-year term, that’s $168,000 regret

- Over a 3-year term, that’s $504,000 regret

What this means:

Even a modest 20% drop becomes a half-million-dollar hit on a 3-year commitment.

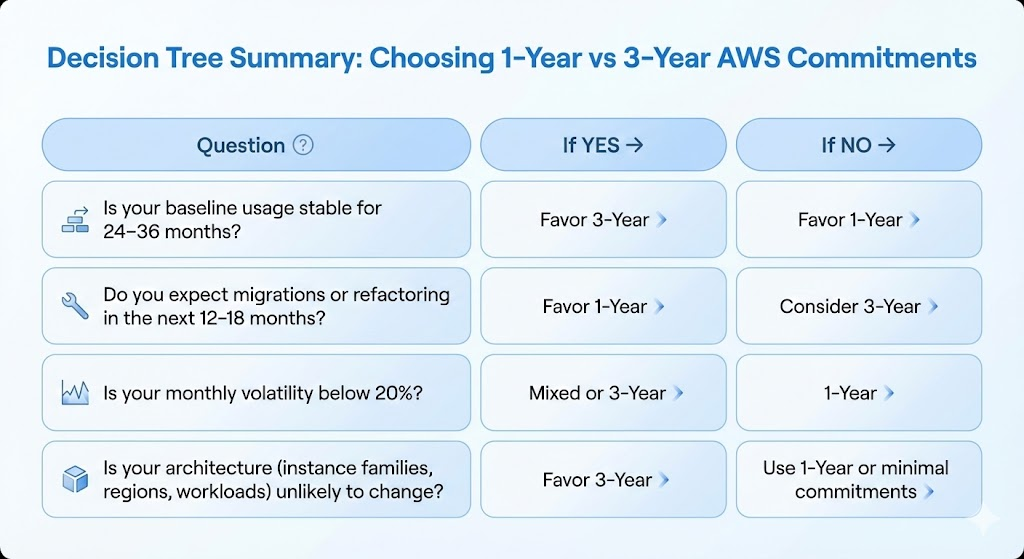

To make the regret curve actionable, here’s a simple decision tree you can use to determine whether a 1-year or 3-year AWS commitment is safer for your environment.

Where Usage.ai Fits Into Your Commitment Strategy

Choosing between 1-year and 3-year AWS commitments becomes far easier once you understand volatility, coverage, and regret. But even with careful modeling, the decision still carries one unavoidable challenge: You must commit today based on usage that will change tomorrow.

This is where Usage.ai adds meaningful risk protection. Usage.ai is designed specifically to eliminate commitment uncertainty by combining:

1. Commitment Automation (Updated Every 24 Hours)

Usage.ai recalculates your optimal commitment coverage daily, using your real usage patterns. This reduces the risk of committing too much or too early because your coverage continuously adjusts to match actual demand.

2. Flex Commitments (SP/RI-Level Discounts Without Long-Term Lock-In)

Flex Commitments are structured to give customers SP/RI–level savings while avoiding long-term inflexible lock-in.This removes the tension between wanting higher discounts and avoiding multi-year regret.

Learn more about Usage.ai’s Flex Commitment Program

3. Cashback Protection (Real Money Back When Usage Drops)

If your usage drops and you under-utilize commitments, you get cashback, turning what would normally be a financial penalty into a reimbursed event. This fundamentally changes the risk equation.

4. Fees Only on Realized Savings

Usage.ai only charges based on actual savings delivered, and not projections.This ensures all incentives are aligned with measurable financial outcomes.

5. Mathematical Modeling Built-In

Everything covered earlier in this article, from volatility analysis, coverage forecasting, risk-adjusted modeling is handled automatically by the platform. Instead of manually working through spreadsheets, Usage.ai evaluates your footprint continuously and adjusts recommendations in real time.

If you’re interested in running a POC, we’d love to show you what safe, automated, cashback-protected savings can look like in your environment. Sign Up now.

Conclusion

Choosing between 1-year and 3-year AWS commitments is ultimately a balance of stability, volatility, architectural change, and financial risk tolerance. Discounts matter, but they matter far less than your ability to consistently consume the commitments you buy.

The math shows that stable workloads benefit from deeper, longer-term discounts, while evolving or unpredictable workloads gain more from shorter terms and flexible commitment strategies. And as your architecture evolves, the risk profile of your commitments naturally shifts with it.

In practice, the best commitment strategies are never “set and forget.” They are continuous, data-driven, and grounded in a clear understanding of how your usage behaves.

Frequently Asked Questions

1. Is it better to choose a 1-year or 3-year AWS Savings Plan?

It depends on stability. Stable workloads benefit from 3-year terms, while changing or volatile environments are safer with 1-year commitments.

2. Do 3-year AWS commitments really save more?

They offer higher discounts, but only save more if your usage stays consistent. If usage drops or changes, the savings can disappear quickly.

3. Can 1-year AWS commitments still deliver good savings?

Yes. They offer meaningful discounts with much lower risk and are often the best choice for teams expecting architectural or usage changes.

4. Why are 3-year AWS Savings Plans considered risky?

They lock you into a fixed commitment for 36 months. If your usage or instance types change, you pay for capacity you no longer use.

5. How do I know if a 3-year commitment is safe?

It’s safe if your expected usage remains above the break-even level for the discount and your workload is stable for the next 2–3 years.

6. What happens if I underuse an AWS Savings Plan?

You still pay for the committed amount, even if you use less. This creates an under-utilization cost that can accumulate over time.

7. Should fast-growing companies avoid 3-year commitments?

Typically yes. High growth, frequent pivots, and evolving architectures make long-term commitments more likely to create regret.

8. Are mixed-term AWS commitment strategies effective?

Yes. Combining 1-year and 3-year terms lets you capture discounts on stable workloads while keeping flexibility for volatile ones.

9. Do migrations impact AWS Savings Plans?

Yes. Migrations often cause temporary usage drops or instance changes, which can make existing commitments unusable.

10. How does Usage.ai reduce commitment risk?

Usage.ai adjusts recommendations daily, offers SP/RI-level discounts without lock-in, and provides cashback protection when usage falls.